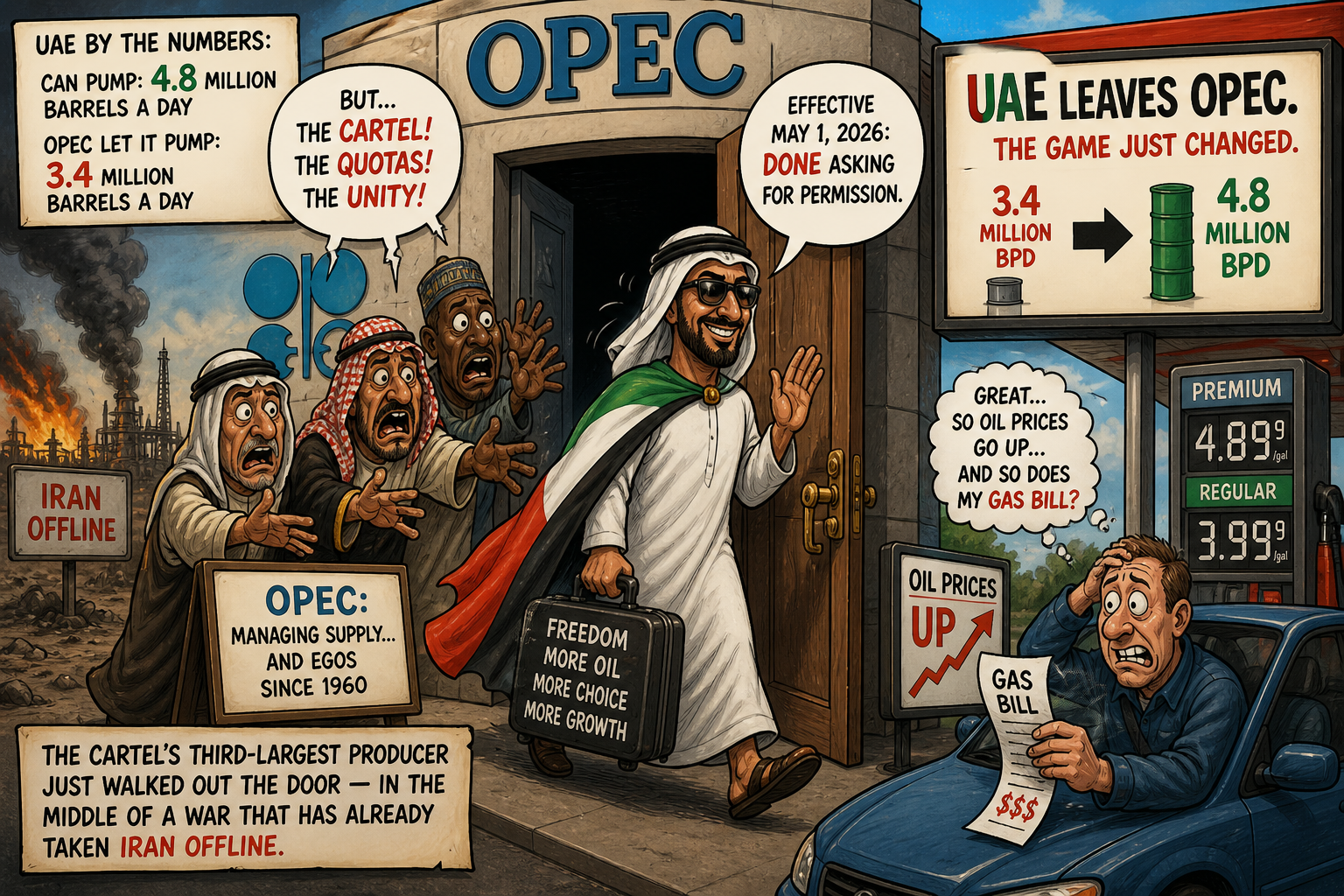

UAE Leaves OPEC.

Here Is What That Means for Oil Prices — and Your Gas Bill.

Abu Dhabi can pump 4.8 million barrels a day. OPEC only let it pump 3.4 million. Effective May 1, 2026, the UAE is done asking for permission. The cartel's third-largest producer just walked out the door — in the middle of a war that has already taken Iran offline.

“The UAE will act in its national interest.”

On April 26, 2026, UAE Energy Minister Suhail Mohamed al-Mazroueinotified the OPEC Secretariat in Vienna that the United Arab Emirates would withdraw from both OPEC and the broader OPEC+ alliance effective May 1, 2026. The decision, al-Mazrouei said in a statement carried by Al Arabiya, was “final and sovereign.”

The trigger, by every account, was the capacity math. The UAE's national oil company ADNOC has spent more than $150 billion over the past decade expanding production infrastructure. Today it can pump 4.8 million barrels per day. OPEC's quota system had capped the UAE at approximately 3.4 million barrels per day— meaning Abu Dhabi was paying to maintain infrastructure it was forbidden from running at full capacity, shipping its restraint as profit directly to Saudi Arabia's balance sheet.

That math had been quietly explosive for years. The Iran war made it politically unsustainable.

1.4 million barrels a day — caged.

The gap between what the UAE could pump and what OPEC allowed it to pump was roughly 1.4 million barrels per day — at current Brent prices north of $100/barrel, that is approximately $51 billion per year in revenue the UAE was leaving on the tableto preserve a cartel agreement that increasingly favored Saudi Arabia's production math over Abu Dhabi's.

ADNOC's expansion program targets 5 million bpd by 2027 and a longer-run ceiling of 6 million bpd — numbers that would make the UAE the third-largest oil producer on earth, behind only Saudi Arabia and Russia. None of that plan was compatible with OPEC membership.

“This takes a real tool out of the group's hands.”

Jorge Leon, Senior Vice President, Rystad Energy — on UAE's OPEC exit

Abu Dhabi opens the taps. Starting May 1.

With the quota gone, ADNOC will ramp toward its 4.8M bpd ceiling immediately. The ramp is not instantaneous — reservoir management, pipeline logistics, and tanker contracts mean the actual production increase happens over weeks, not days. But the direction is unambiguous. Analysts at S&P Global Commodity Insights estimate the UAE can add 800,000 to 1.2 million bpd of effective daily output within 60 to 90 days.

For context: that incremental supply alone is larger than the entire daily output of Libya. It is roughly equal to the production gap created when Iran's export capacity was knocked offline in the February 2026 strikes. The UAE's decision is, in effect, a unilateral rebalancing of global supply at a moment when every barrel is politically load-bearing.

Energy Minister: Suhail Mohamed al-Mazrouei — delivered the withdrawal notice to Vienna.

ADNOC CEO: Sultan Al Jaber — overseeing the production expansion program; also UAE Special Envoy for Climate and former COP28 President-Designate.

Saudi Arabia is now doing the heavy lifting alone.

The UAE was OPEC's third-largest producer. With Iran already offline from the war and the UAE now gone, OPEC's effective market-share control falls from roughly 30 percent of global supply to closer to 26 percent— the lowest in the organization's 65-year history.

Saudi Arabia is left as the effective sole swing producer with both the will and the capacity to enforce discipline. Riyadh had already been carrying disproportionate production cuts to hold prices above the $80-$85 floor Saudi Arabia needs to balance its domestic budget. Without Abu Dhabi's compliance — and with the UAE now actively flooding the market — that balancing act becomes exponentially harder.

Qatar left OPEC in 2019, calling the organization politically ineffective. The UAE's departure is historically larger: no country of the UAE's production weight has ever left. It is the largest single-member exit in OPEC's history.

The UAE can pump more. The strait is still contested.

Here is the near-term constraint that every analyst agrees on: the UAE cannot ship what it cannot get out. Roughly 85 percent of UAE crude exports move through the Strait of Hormuz. The strait is currently contested — U.S. naval assets are enforcing a partial blockade, Iranian underwater mines laid before the February strikes are still being cleared, and tanker insurance premiums through the chokepoint have risen more than 900 percent since the war began.

The UAE operates one significant Hormuz-bypass pipeline: the Abu Dhabi Crude Oil Pipeline, which runs 370 kilometers to Fujairah on the Gulf of Oman — outside the strait. That pipeline has a rated capacity of approximately 1.5 million bpd. It is the only major escape valve. This means even at full production expansion, roughly half of UAE exports remain Hormuz-dependent until the strait is fully cleared.

The full supply benefit of the UAE's departure — the 1.4M bpd unlocking global markets — is real, but it arrives in stages as the security situation resolves. The market knows this. Brent crude is holding above $100/barrel despite the announcement, down from its war-shock peak but still elevated. Traders are pricing in the future supply while discounting how fast it can actually move.

The Abu Dhabi Crude Oil Pipeline (ADCOP) — 370 km from Habshan to Fujairah — has a rated capacity of ~1.5M bpd, bypassing the Strait entirely. Current UAE production: ~3.4M bpd pre-exit. After ADCOP accounts for 1.5M, approximately 1.9M bpd still must transit Hormuz. Full bypass of the strait requires either the security situation to resolve or ADCOP expansion — the latter is in ADNOC's long-term plan.

$20 billion. An Iron Dome. A very specific alignment.

The UAE's OPEC exit does not happen in a geopolitical vacuum. In the weeks surrounding the departure announcement, the U.S.–UAE relationship has moved with unusual speed and specificity:

- →Treasury Secretary Scott Bessent signed a $20 billion bilateral economic cooperation framework with Abu Dhabi, structured as a currency swap line and infrastructure co-investment vehicle.

- →The U.S. deployed an Iron Dome air defense battery to UAE soil, the first such deployment to a Gulf Arab state — specifically in response to Iranian drone and missile attacks on Abu Dhabi during the Iran war's opening phase.

- →UAE officials were briefed by CENTCOM on the Iranian naval mine-clearing timeline in the strait — suggesting Washington wants Abu Dhabi's production to move as fast as logistics allow.

This is the petrodollar alignment in 2026 form: the UAE exits an organization that was throttling its revenue, receives U.S. security guarantees and capital, and begins pumping at full capacity into a market the U.S. wants to keep from going to $150/barrel. Iran and Saudi Arabia, the two countries most damaged by this arrangement, share an opponent for once — though for entirely different reasons.

“The UAE has concluded that its security and its economy are better served outside OPEC than inside it.”

Suhail Mohamed al-Mazrouei, UAE Energy Minister, April 26, 2026

Gas is $4.18 nationally. Here is where it could go.

The U.S. national average for regular gasoline on April 28, 2026 is $4.18 per gallon — elevated from the pre-war $3.40s by the Hormuz disruption, the Iran supply shock, and war-premium insurance costs baked into every barrel that transits the Gulf.

The UAE's full production ramp-up, once it flows through Hormuz or the ADCOP bypass, would add roughly 1.4 million barrels per day of net new non-OPEC-restricted supply to a market that was underallocated after Iran went offline. EIA modeling places the eventual price impact in a $8 to $15 per barrel downward pressure range on Brent once the UAE supply is fully flowing — which, depending on Hormuz clearance timelines, is 60 to 120 days out.

Translated to the pump: that's a 20 to 35 cent per gallon decline over Q3 2026, assuming no new supply disruption. Not a return to $2.80. But a real, measurable reduction.

How OPEC lost its third-largest producer.

The UAE spent $150 billion building oil infrastructure OPEC wouldn't let it use. After Iranian missiles hit Abu Dhabi, the calculation changed. The exit is permanent. The supply is real. The question is only when it clears the strait.

OPEC loses its third-largest producer at the worst possible moment for the cartel — with Iran offline, Saudi Arabia overextended, and global consumers desperate for supply relief. The UAE is betting that its expanded production, combined with U.S. security guarantees and capital, builds a better future outside a quota cage than inside one. The market will tell us if they're right. So will the price at the pump.

All figures cite primary sources: ADNOC official press releases, OPEC Secretariat communications, EIA Short-Term Energy Outlook, U.S. Treasury and CENTCOM statements, and wire-service reporting (Reuters, Bloomberg, Financial Times). Price projections cite EIA and Rystad Energy modeling, noted as forward-looking estimates. Barrel-per-day figures represent official capacity ratings and OPEC quota allocations.